.png?width=69&height=53&name=Acrisure%20Logo%20(White%20Horizontal).png "Acrisure")

CHRIS DALY

HNI Vice President

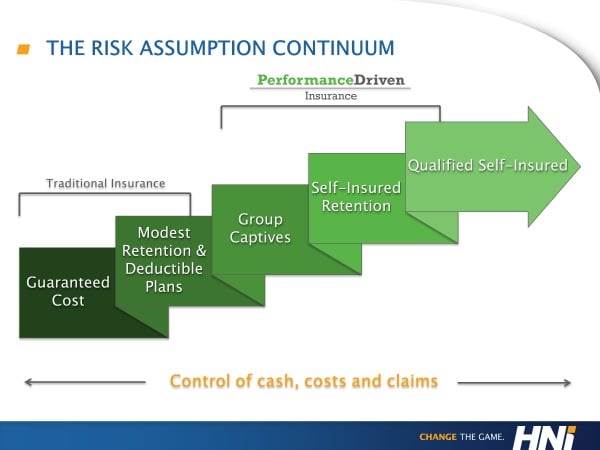

Successfully managing risk assumption and controlling costs are important objectives for all companies. However, the manner in which a company goes about achieving these objectives varies depending on size, predictability of losses, risk management abilities, and financial strength.

The diagram below helps to illustrate different insurance options. Where are you on the Risk Assumption Continuum? There are no right or wrong answers; this tool will help you understand your current state and provide insight on what elements need to be in place to move along the continuum.

Traditional Insurance Models for Risk Assumption

In these models (Guaranteed Cost and Modest Retention & Deductible Plans), the insured pays a premium and most (if not all) risk is transferred to the insurance company. Costs are fairly predictable in these programs, which helps with budgeting. However, costs can move up and down with swings in the insurance market. Loss experience and partnering with the right insurance company is key to maintaining stable costs in these programs.

Performance-Driven Insurance Models

The following offer insureds the opportunity to have their insurance costs tied more closely to their loss experience. With such plans comes both risk and reward.

Group Captives

Insureds are able to assume a larger portion of risk than traditional insurance by working collectively with other like-minded companies. The performance of the individual and group as a whole dictates ultimate costs. Expected cost of losses are pre-funded, and in good years, excess premiums may be returned in the form of dividends. In short, with greater risk comes potential for greater reward. A captive also helps to insulate buyers from cyclical changes in the insurance market.

Self-Insured Retention

This structure allows insureds to stand on their own performance rather than with a group. Because they stand on their own, insureds' costs become a true reflection of their own performance. Premiums generally are lower than other models and losses within the retention are paid as you go rather than pre-funded, offering a significant cash flow benefit to insureds. This program promotes stable costs as buyers are fairly well insulated from volatility in the insurance market.

Qualified Self-Insured

Risk is no longer transferred to another entity. The insured is responsible for losses from the ground up, although most will elect to buy excess coverage at some point. The insured is responsible for all claims management and costs of claims. High confidence in risk management and predictability of loss is a must. The end result? Your costs equal your claims, along with the commodity cost of any excess coverage.

Remember progression along the Risk Assumption Continuum is not intended to be a path toward cheaper insurance, but lower overall costs should be expected. That's because safety efforts drive the expected outcome.

Each firm is unique and faces unique risks. Just because you're in one spot on the continuum doesn't mean that's your final destination. With hope, this Risk Assumption Continuum gets you thinking about where you want to go and how you might start thinking differently to get there.

![Captivate Your Employee Benefits [Get the Event Materials]](https://no-cache.hubspot.com/cta/default/38664/411a649a-1b21-486e-a584-f390c2a5a6d4.png)

Related Posts:

The 5 Biggest Myths about Captive Insurance